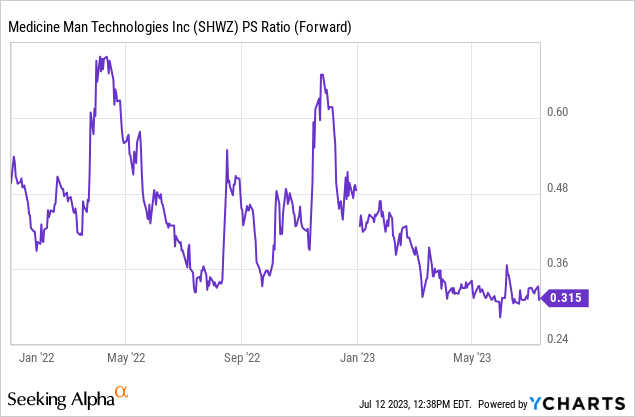

Medicine Man Technologies (OTCQX:SHWZ) forms one of the smaller and less covered US multi-state operators, with a $56.7 million market cap and an over-the-counter listing that has broadly limited its investor base. The Denver-based company is down 26% since the start of 2023 and is now trading hands at a 0.34x price-to-sales multiple, with $167.6 million in trailing 12-month revenue for its fiscal 2023 first quarter. Medicine Man, operating as Schwazze, is now trading at its lowest-ever sales multiple as negative market sentiment towards a so-far lackluster North American cannabis industry gets compounded by a Fed funds rate at its highest level in over a decade at 5% to 5.25%.

Schwazze owns 10 cannabis brands from New Mexico medical and recreational cannabis dispensary R. Greenleaf, research and development outfit Schwazze Biosciences, and Colorado pure CO2 and ethanol extractor Purplebee’s. The bull case here is built around US recreational cannabis sales, forecasted to grow to reach $71 billion in 2030 even without federal legalization. It’s not hard to why Schwazze’s bulls against this forecasted market size continue to hope for a recovery.

A Recovery That Could Be

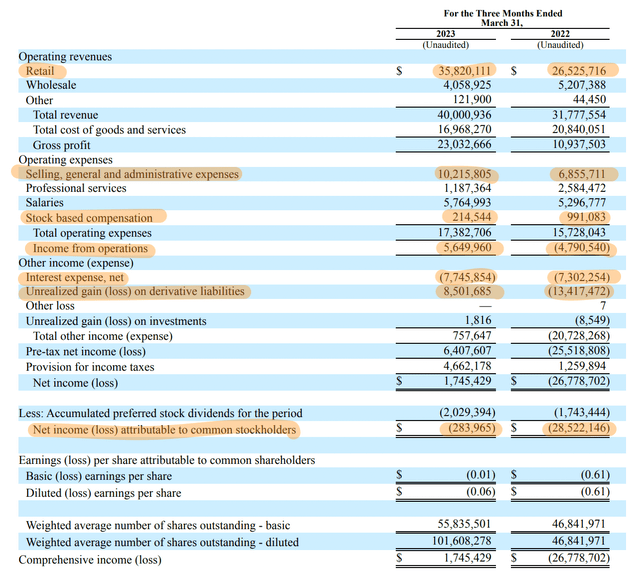

A few things have to happen for Schwazze to stage a recovery, the most important of these coalesce around the company’s liquidity position and operational momentum amidst a highly discombobulated cannabis market. Firstly, the cannabis company has to be able to maintain revenue growth that came in at 25.9% for its first quarter. This year-over-year growth rate meant revenue of $40 million, a miss by $1.17 million on consensus estimates. This was driven by retail sales that grew by $9.3 million to $35.8 million on the back of Schwazze’s dispensary store footprint in New Mexico and Colorado expanding to 60 as of the end of the quarter. The company has been quite aggressive on this front, acquiring two retail outlets and a medical dispensary in Colorado. In New Mexico, Schwazze acquired 14 retail outlets, one manufacturing, and one cultivation facility during the first quarter.

Medicine Man Technologies Fiscal 2023 First Quarter Form 10-Q

The strategy is to build on their position in Colorado and New Mexico, breaking with the broader cannabis sector zeitgeist of asset sales, radical cost reduction initiatives, and extreme cash conservation. SG&A expenses for the quarter grew by 49% year-over-year to reach $10.22 million, even as other operating expenses like stock-based compensation and professional services saw marked declines versus their year-ago comps. Schwazze was able to realize income from operations of $5.65 million which when set against interest expense of $7.75 million and some other non-cash items including an $8.5 million unrealized gain on derivative liabilities drove a $284,000 net loss for the quarter attributable to common stockholders.

Schwazze’s Cash Runway

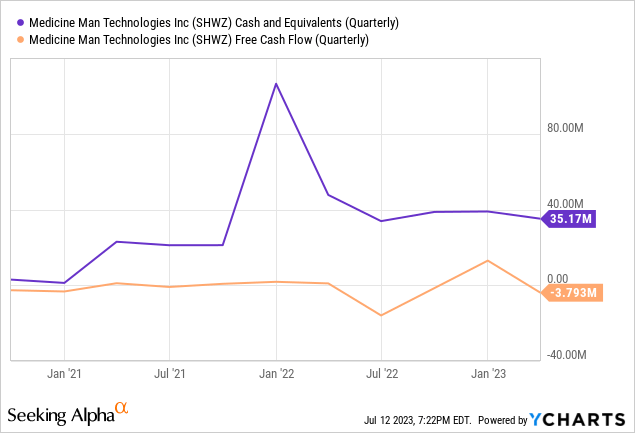

The company’s cash and equivalents as of the end of the quarter was $35.17 million, down sequentially from $39.4 million in the fourth quarter and from $47.7 million in the year-ago period. This came against a free cash outflow of $3.8 million during the quarter. What’s odd is the first quarter earnings press release and subsequent earnings call both say that Schwazze generated $2.7 million in free cash flow, with the company using its own non-GAAP measure for this that adds back cash interest expense. Schwazze held total debt of $131.2 million as of the end of the first quarter, up $3.4 million from the year-ago comp, as the company sees through its expansion strategy. This is a broadly unhelpful metric from an investor’s perspective that impacts comparability with peers.

If we adjust Schwazze’s market cap for its debt and cash position as of the end of the first quarter, we should arrive at an enterprise value of around $152.73 million. This would form an enterprise value to trailing 12-month sales multiple of 0.91x, a metric that is more reflective of the high debt balance of Schwazze. The risk here is that continued GAAP free cash outflows in future quarters get aggregated to restrict the company’s cash runway. The company currently has enough cash to maintain operations for around ten quarters without further external capital.

Hence, Schwazze will need to raise more funds. This could prove to be a difficult task against a stock price that’s lost so much value over the last three years. A broad stock market recovery on the back of a future interest rate cut now seems to be the most likely near-term event for bulls to look forward to. This cut could come in the first half of next year, with the remainder of 2023 set to see the commons continue to trade broadly flat. I don’t have a position here, but the stock is likely a hold against this.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here