I was planning for some kind of falling knife image. However, the tool opened to images of cookie dough. I think we can all agree this image is better.

Share prices have fallen hard. No disputing that. But I still believe in these shares. Thankfully, many of my purchases have been around the lower end. Unfortunately, “many” is dramatically different than “all”.

If you find falling knives as unappealing as a Justin Beiber concert, you’ll want to read one of my other articles instead. But you won’t be spoiled for choice. I’m focused on great REITs where prices plunged.

If you were looking to buy a rental home, wouldn’t you be interested in the house that sold for $600k a year ago and just got offered for $450k? You’d at least call a realtor and ask if something was wrong with it, right? That would be a potential bargain.

Real Estate Values

But replace the real estate (rental home) with a REIT and it becomes the dreaded “falling knife”.

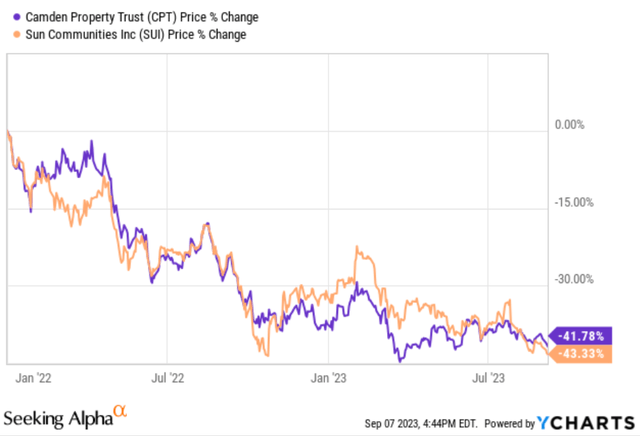

YCharts

Thanks to the remarkable lag between transactions happening and data being released, we can now say that home prices increased again in June 2023. That’s another 5 consecutive months of home prices increasing.

Did I predict that string of rising home prices? No, absolutely not. That’s a surprise to me.

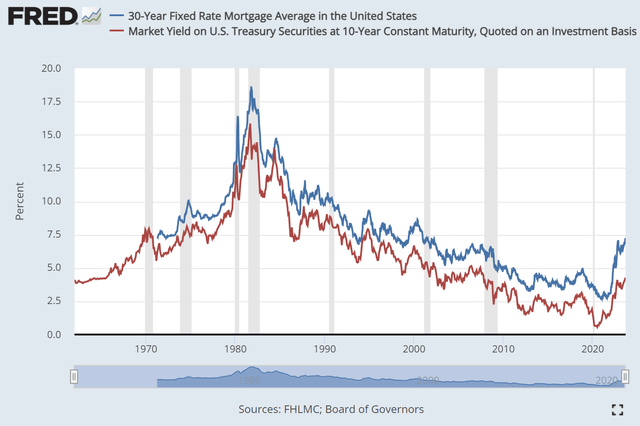

Mortgage rates soared higher. While 10-year Treasury yields increased, they didn’t increase nearly as much as mortgage rates:

Federal Reserve

That surge in mortgage rates made homes vastly less affordable.

Inflation was already painful, but higher interest rates meant homes come with high prices and high-cost financing.

Yuck.

Interest Rates

Fortunately, Treasury yields climbed slightly before mortgage rates. That triggered me to write this section in our Portfolio Update for early September 2021:

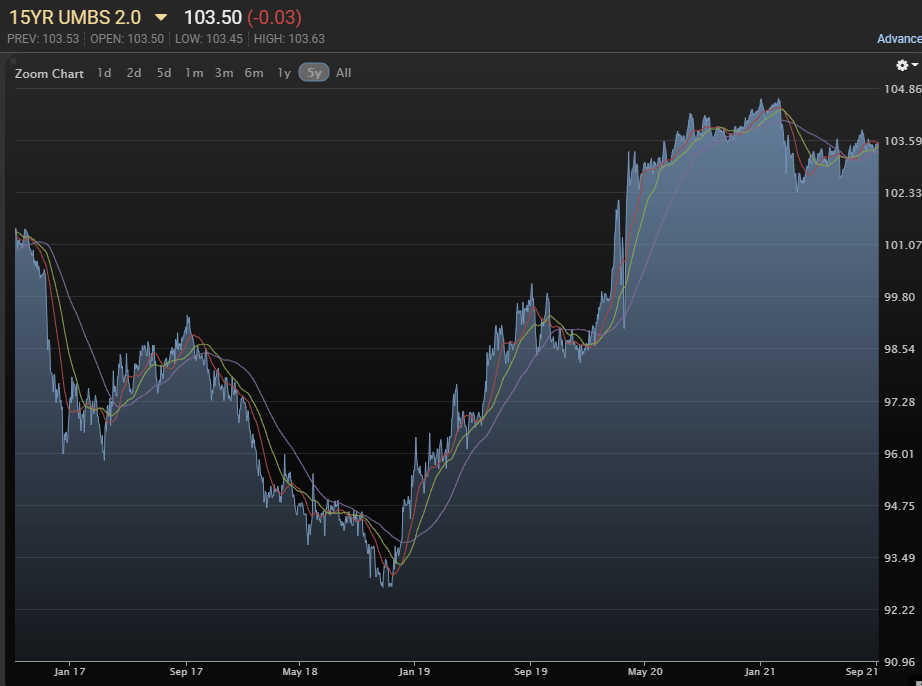

Another part of the picture worth highlighting is the appeal of refinancing. Prices for agency mortgage-backed securities are pretty strong. If someone didn’t refinance in late 2020, this is a reasonable time to do so. See the chart below showing the daily prices on a 15-year fixed-rate agency MBS with a coupon rate of 2%:

MBSLive

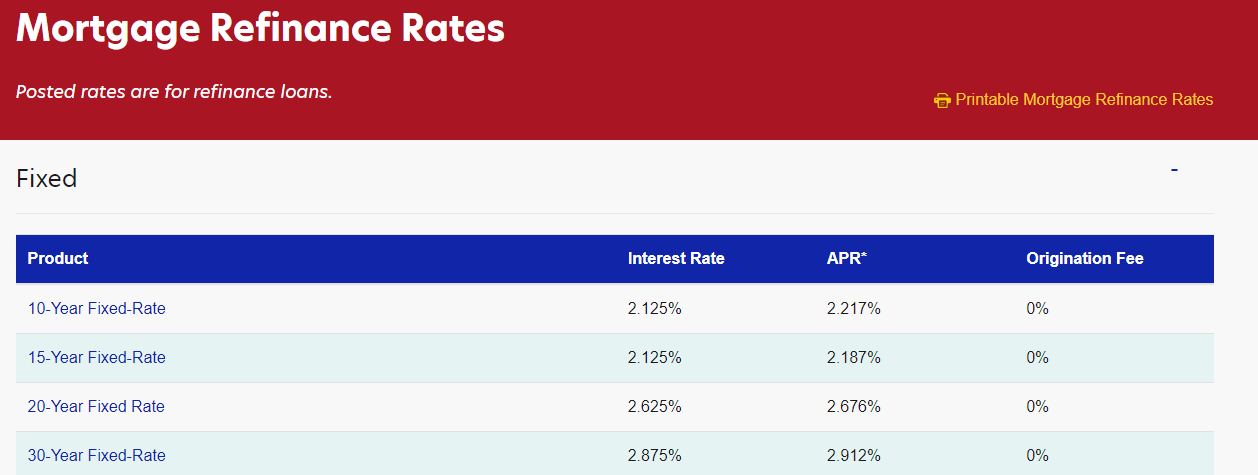

Those mortgages are selling at 3.5% over face value. That’s enough for homeowners to be able to get an attractive rate on refinancing. I filed my paperwork, began the process, and already locked the rate. In my experience, going through a local credit union has resulted in a better experience and competitive pricing. To give investors a quick frame of reference, these are the current rates from my local credit union:

Ent Credit Union

Refinancing won’t make sense for everyone, but for those with an interest rate above 3% and the ability to switch into a 15-year loan, it could result in healthy savings.

In hindsight, that encouragement for members to refinance looks great. Anyone using that idea saved vastly more than our membership fees.

As usual, I followed my own suggestion. I refinanced my house to lock in 2.125% on a 15-year mortgage. That made inflation and rising rates far less painful.

For people trying to buy a home today, it’s dreadful.

The hottest market is Miami. Sorry, bad pun. Sorry. How are homeowners able to afford such high mortgage rates? Well, nearly 40% of total sales were cash purchases. That compares to the national average of 26%. Sorry, I did say “homeowners”. Well, they own somebody’s home!

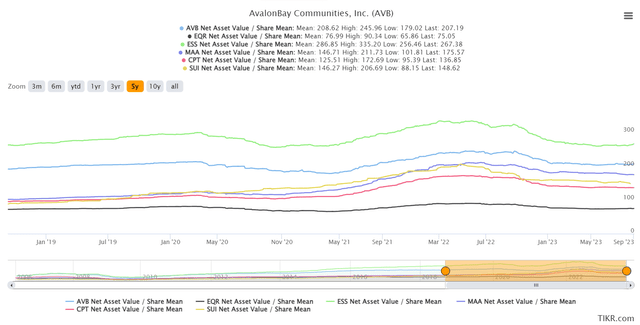

REIT Net Asset Value

Okay, so home prices are going up. How about other forms of housing like apartments and manufactured housing parks? Those are also housing. Investors are clearly buying single-family homes (sorry, working-class buyers rarely pay cash). So investors want other residences they can rent out, right?

Well, here’s the trend in NAVs (Net Asset Value):

TIKR.com

The chart covers AvalonBay (AVB), Equity Residential (EQR), Essex Property Trust (ESS), Mid-America Apartment (MAA), Camden Property Trust (CPT), and Sun Communities (SUI).

Unfortunately, I can’t normalize the chart. Consequently, lines near the top of the chart have to move further to generate the same percentage change. The point is that you can see a trend higher going into 2022, then a trend lower since summer 2022.

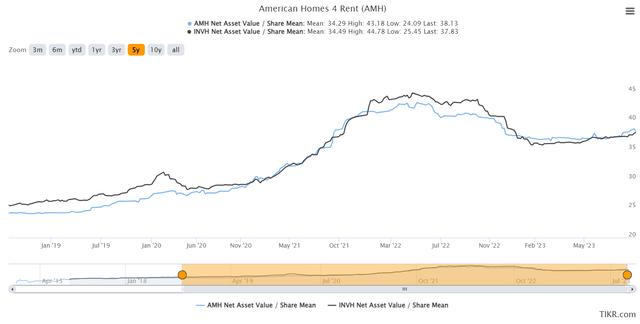

Was the issue really the type of assets? Maybe it’s just because everything except for detached single-family homes is trash that no human being would ever want to live in. If that’s the issue, then REITs that own single-family homes probably saw their NAV’s continue to rise, right?

TIKR.com

That chart is American Homes 4 Rent (AMH) and Invitation Homes (INVH).

Look at that, it’s a similar chart! Who would’ve guessed? Individual home prices went up, but a broadly diversified basket of them clearly went down significantly. Even if we adjust for leverage, this says the asset values fell around 8% to 10%. That’s a rough estimate. Eyeballing it and adjusting for leverage.

The Risks

There are three major risks for housing REITs today.

Recessions are bad. That’s just how things go. They are bad. People lose their jobs and move in with their parents.

Interest rates are still elevated. The yield curve has become slightly less inverted as longer-duration Treasury yields rose even more than short-term rates. This is still a challenge for affordability.

Supply is coming. Many people are angry about rent increases, but their movement may lose steam as new supply hits the market in 2024. Rent growth should stall out. Some markets will require incentives (like free weeks of rent) to maintain occupancy as new units hit the market.

The market hates REITs that see a temporary dip in growth for FFO and AFFO per share. Consequently, that new supply on the horizon can be scary. On the other hand, the REITs are trading at significant discounts to the fair market value of their assets.

One of the things I find interesting here is the way the issue with supply will likely play out. It may appear to protestors that they are succeeding in stopping rent growth. The real factor is the increase in supply. The supply was fueled by severely negative real interest rates in 2021. As interest rates ripped higher, new apartment starts plunged. Around 2026 there will be a massive “shortage” of apartments. That’s because new development activity is plunging.

The solution to the housing “shortage” comes in two parts:

Encourage negative real rates.

Allow developers to build new apartments.

Many people hate both parts of this solution. That’s why new housing construction tends to be weak.

Investment Implications

I still like the valuation on apartment REITs and manufactured housing REITs. I expect to see significant headwinds to FFO and AFFO per share from the surge in supply. However, valuations include significant discounts to net asset value and attractive AFFO multiples. My biggest position in the sector is SUI. It comes in at just over 7% of my portfolio. At $119, I think shares are an outstanding deal. I reviewed SUI’s valuation more in my latest Portfolio Update (also published today).

7% in one REIT is simply too concentrated for many investors. I agree. No argument here. But… analysts should eat their own cooking. If an analyst won’t put their wealth on the line, why would you care about their opinion?

I also have positions in AVB, CPT, and ESS. I might add to any of my four housing REIT positions or start a position in one of the other apartment REITs. There are several nice opportunities in the sector for long-term income investors. Yes, the yields are lower than current 3-month Treasury yields. However, the REITs offer growth without requiring the dividends to be reinvested. By the time 3-month Treasury yields fall, we could be looking at higher prices.

I’m not trying to pick the bottom, just finding good deals on great companies.

Lakin, ikramiyelerin şartlarını dikkatlice incelemek ve idrak etmek değerlidir. İnternet bahis platformlarında isimsiz katılmanın tek farklı faydası, çeşitli oyun çeşitlerini deneme imkanıdır. Anonim şeklinde...

Oyun tecrübenizi ekstra eğlenceli şekle getirmek maksadıyla, çeşitli bonus ile teşviklerden istifade edebilirsiniz. Birçok şans oyunları platformu, güncel katılımcılara artı bağlı katılımcılara çeşitli bonuslar...

Один из самых популярных в этой сети – азиатский PokerOK, являющийся одним из лидеров в мировом онлайн-покере. По системе PVI рейк засчитывается покеристу, который...