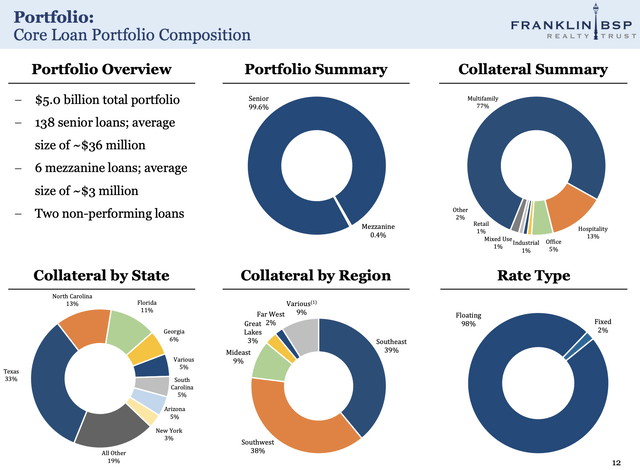

Franklin BSP Realty (NYSE:FBRT) like other mortgage REITs has been fighting the Fed for the last two years with a $5 billion commercial real estate loan portfolio spread across 144 loans as of the end of its recently reported fiscal 2023 fourth quarter. This portfolio is heavy on multifamily loans with a 77% allocation but is diversified across office, hospitality, and industrial properties amongst other property collateral. CRE angst describes deep market fears around a tripartite of headwinds currently faced by US commercial real estate. From the Fed’s own battle with inflation pushing base interest rates to a more than two-decade high of 5.25% to 5.50%, rising office vacancies from working-from-home, and a seesaw economic backdrop. I last covered the ticker in the summer of 2022 with a broadly neutral outlook.

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

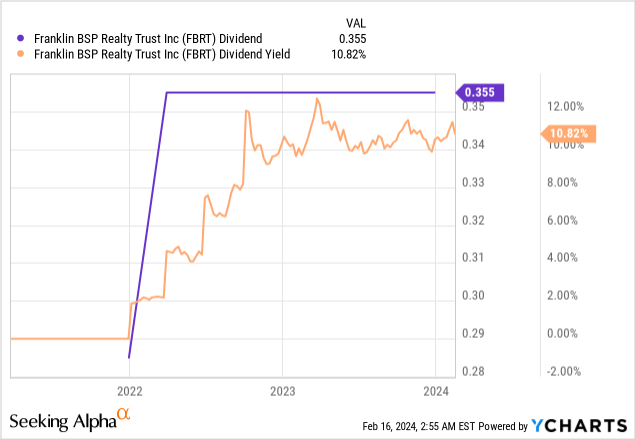

FBRT last paid a quarterly cash dividend of $0.355 per share, kept unchanged sequentially and $1.42 annualized for a 10.8% forward dividend yield. The safety of these distributions against broad CRE angst is the uncertainty for 2024. FBRT loan portfolio only has a 5% exposure to office properties, is 98% floating rate loans, and comes with broad US geographic exposure but with a material allocation to the Sun Belt. The mREIT started trading in 2021 after the merger of Benefit Street Partners Realty Trust and Capstead Mortgage Corporation. Capstead’s preferreds (NYSE:FBRT.PR.E) at the time changed names and remain outstanding.

Originations And Dividend Safety

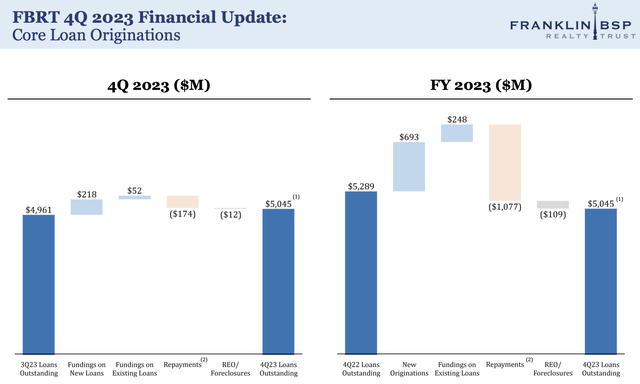

FBRT generated a total income of $263.95 million for its full year 2023, up 27.6% over its year-ago comp but a miss by $4.09 million on consensus estimates. Growth was driven by the year-over-year rise in base interest rates and new originations of $693 million through 2023. FBRT originated $218 million of new loans during its fourth quarter. This was ahead of $174 million in repayments, however, full-year repayments at $1.08 billion were ahead of 2023 originations by $384 million. This led to a dip in loans outstanding but has left FBRT with elevated liquidity which provides security against the turbulent macro backdrop.

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

FBRT had $338 million in unrestricted cash at the end of its fourth quarter, up 88% from $180 million in its year-ago comp to form 5.7% of FBRT’s total assets. The mREIT’s total liquidity stands at $1.5 billion with the inclusion of available financing which management highlighted during their earnings call will be more actively deployed in 2024. They’ve been extremely active with $155 million in loan commitments year-to-date at the time of FBRT’s earning call. They also flagged another $78 million in funding to close in February against a still robust pipeline for the first quarter of their fiscal 2024.

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

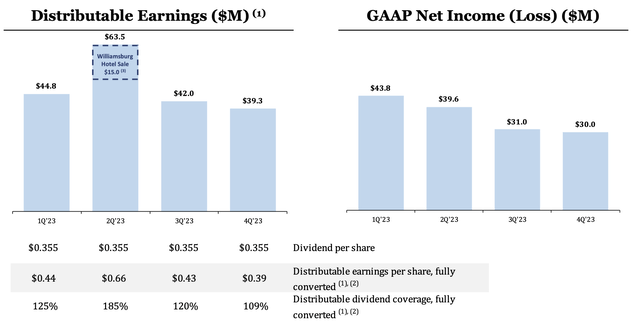

This would put the first quarter ahead of the fourth quarter in terms of new originations as the mREIT tries to strike a balance between playing defense against the specter of a recession and maintaining GAAP net income growth. Net interest income for the fourth quarter came in at $54 million to drive GAAP net income of $30 million. This dipped by $1 million sequentially but grew from $27.2 million in the year-ago comp due to higher base rates. The core risk here is declining dividend coverage. Distributable earnings for the fourth quarter were $39.3 million, around $0.39 per share, down 4 cents sequentially. This meant the $0.355 per share quarterly dividend was 110% covered during the fourth quarter, down from 121% coverage in the third quarter.

Book Value And Credit Quality

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

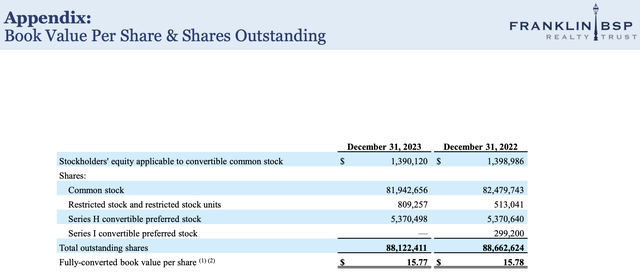

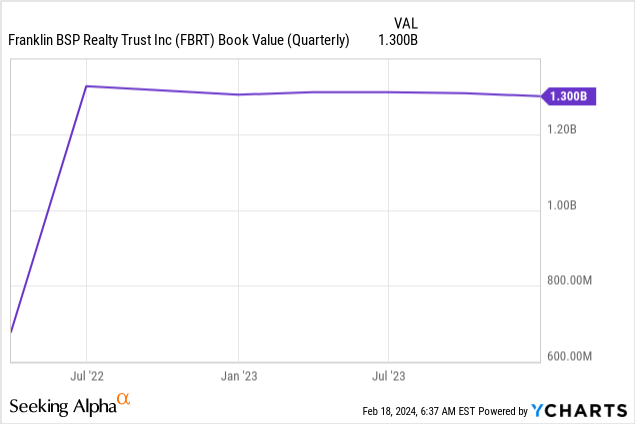

FBRT’s book value per share at $15.77 was down from $15.82 in its third quarter and also dipped by a small 1 cent from its year-ago comp. This means the commons are currently trading hands at an 18% discount to book value. Such a deep discount set opens up current shareholders to possible near-term upside.

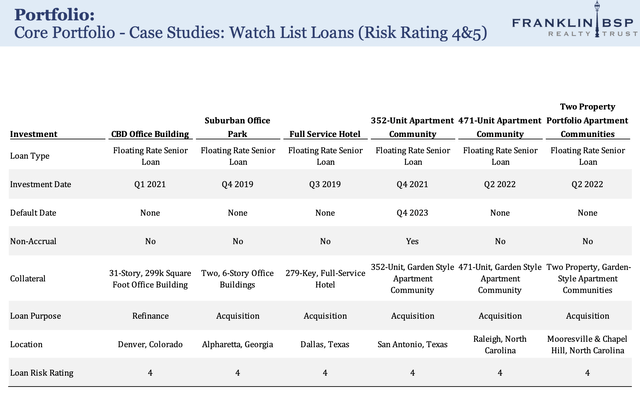

Critically, book value has broadly remained stable since the merger despite the headwinds faced by office properties and multifamily developers from higher base interest rates. FBRT has six assets on its watchlist at the end of the fourth quarter. There are another 3 foreclosure REO positions, around 2% of total assets.

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

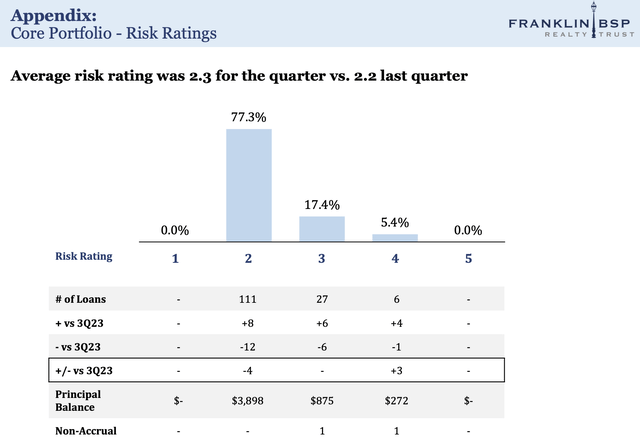

Only one of these watchlist loans, a 352-unit apartment community in San Antonio, is on non-accrual as of the end of the fourth quarter. Further, FBRT incurred no CECL charges during the fourth quarter but increased its general CECL reserve by $5.4 million with the total now 96 basis points of the mREIT’s total portfolio.

Franklin BSP Realty Fiscal 2023 Fourth Quarter Supplemental

Overall, FBRT’s risk ratings are still flashing green with a multifamily focus reducing overall volatility as a sequential ramp-up of loan originations in the first quarter looks set to improve underlying net income and boost declining coverage. FBRT is a buy at its current level with its double-digit dividend yield and large discount to book value forming the reasons for the rating.

Read the full article here