Introduction

Cybersecurity is as essential as drinking water in the digital age, where we are ever more connected and integrated online and exposed to digital criminals that can reap devastation via data ransom, identity theft, and corporate espionage to name a few threats. The virus, malware, and more direct hacking threats were protected via hardware, firewalls, and software installed on your PC. This is now moving (as everything digital) to the cloud and being platformed; i.e. readily available to all of a person or a company’s connections. The age of generative AI can only increase the need to protect our digital world, and hence I am running an analysis on Fortinet (NASDAQ:FTNT), a company that has underperformed in the last 12 months.

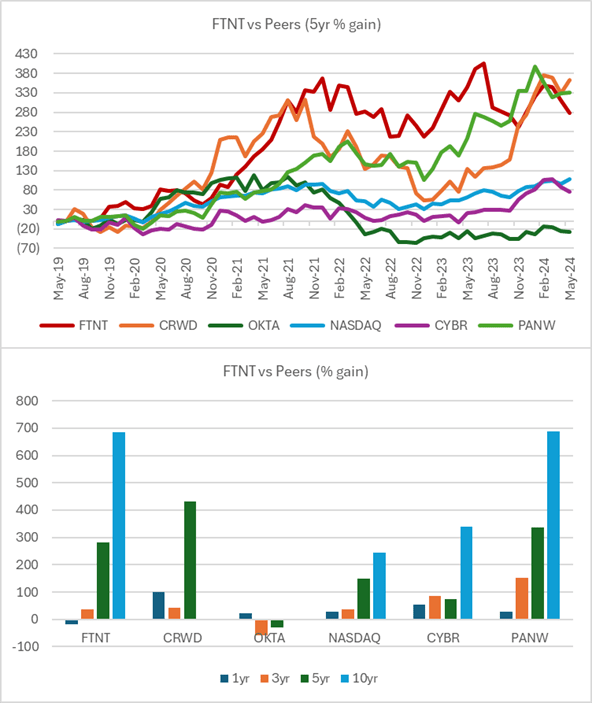

Performance

Until August 2023, at its 2Q23 results report, FTNT had been a solid performer within the Cybersecurity sector. At that time, the company began to cut guidance due to declining sales in its firewall products that continued into 2024 and still plagues consolidated results as well as market perception and valuation. In the last 12 months, the stock has been down 17% with flat 3-year returns.

Created by author with data from Capital IQ & GS

What is Fortinet?

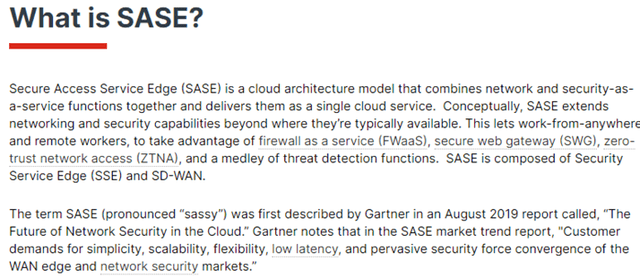

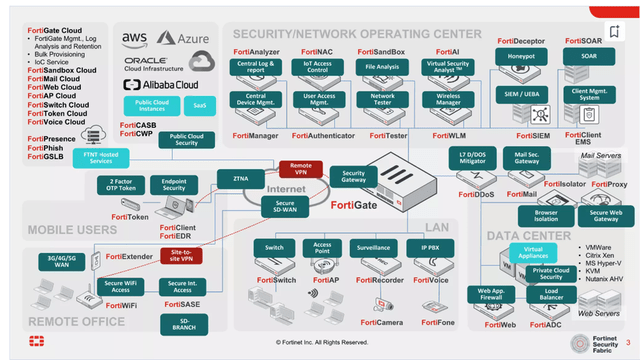

FTNT is a hybrid company, offering both hardware and software products. Fortinet began operations providing firewall devices and has now developed a security software-as-a-service delivered on a cloud platform. The primary growth driver is SASE (pronounced sassy), which extends cybersecurity beyond companies’ infrastructure and allows for secure remote work. In contrast, CrowdStrike (CRWD) offers software via the cloud and Palo Alto (PANW) is also a hybrid player. FTNT’s growth has been hindered since mid-2023 by the normalization of product sales (firewall) post-pandemic spike and a rapid shift by customers and vendors to a more integrated cloud platform that can consolidate services, reduce complexity and costs. In FTNT’s own words, they believe there are too many cybersecurity companies, and consolidation should take place. Below I provide excerpts of FTNTs products for reference.

FTNT FTNT

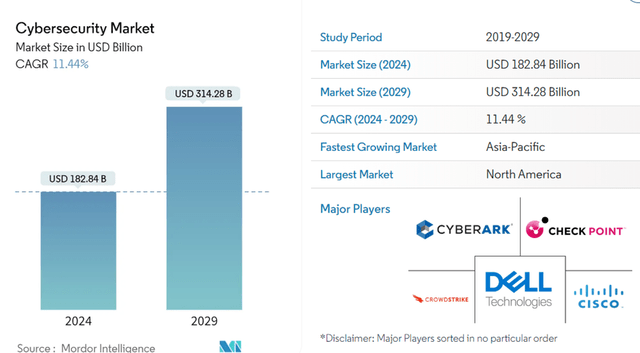

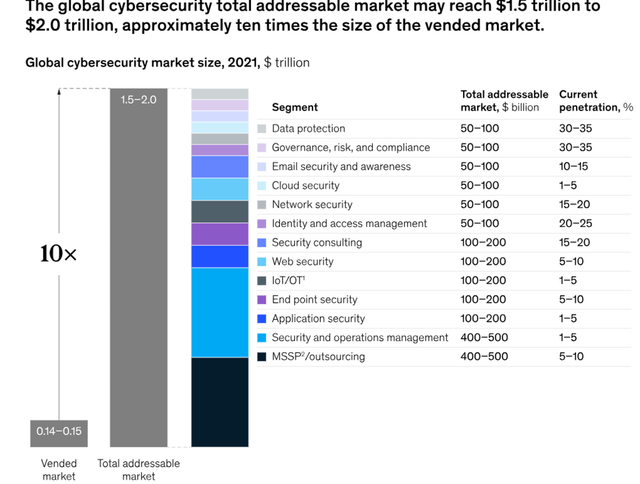

The Cybersecurity Market

This size and growth of the cybersecurity market are well known by most investors. The advent of the cloud, hyperscaler penetration, and now AI is shifting customer preferences, as mentioned earlier, away from on-premise infrastructure to platform services. While the size and growth of the market may not change, the companies providing this service are likely to do so. Below are excerpts of two studies that indicate revenue growth of around 12%, this means that some products/services will grow at twice that rate, and others will decline.

Mordor Intelligence

Mckinsey

Consensus Forecasts

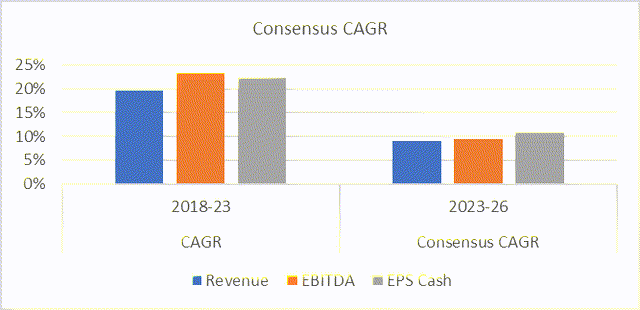

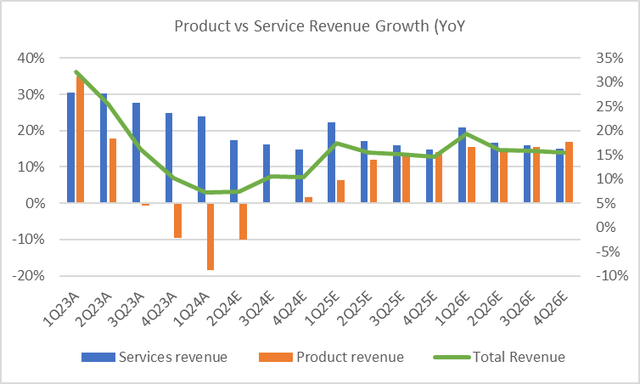

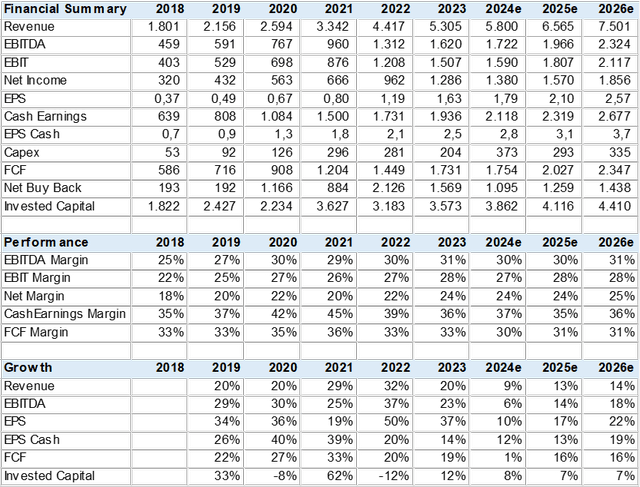

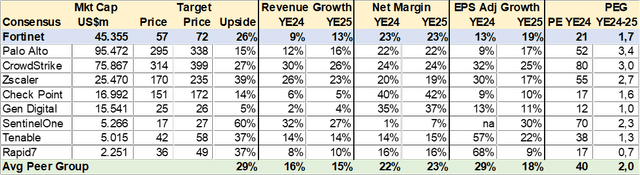

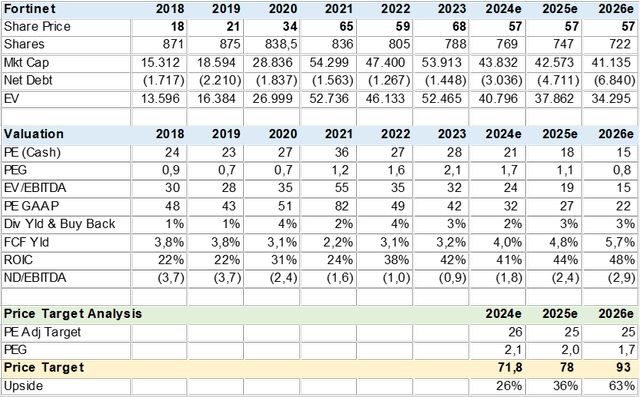

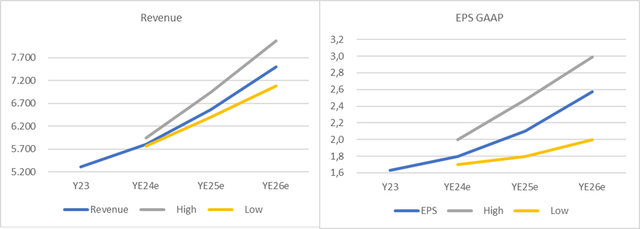

I am using consensus data from 36 analysts to gauge growth, profitability, and valuation. As mentioned earlier, the company has experienced a deceleration of revenue and earnings since mid-2023 that has impacted forward estimates. In the 2018-2023 period, FTNT saw over 20% EPS (cash) CAGR, while estimates to 2026 are half this. This dip in growth is weakest in 2024 with an estimated 9% top-line increase and 12% EPS due to declining product revenue estimated to endure through 2024 and most of 2025 according to a research note from Goldman Sachs.

According to consensus, this slower growth should have a modest impact on margins due to the high growth in services that carry better overall margins. What could be considered worrisome is that FTNT is not projected to regain its past 20% growth rate in cash EPS (GAAP EPS is higher according to Seeking Alpha data) which may be due to competitive reasons, i.e. being late to cloud-based services or due to its relative size within the market that makes it difficult to gain share.

FTNT Consensus Growth (Created by author with data from Capital IQ) FTNT Revenue Growth Breakdown (Created by author with data from Capital IQ &GS) FTNT Consensus Estimates (Created by author with data from Capital IQ)

Peer Comps

I gathered consensus data for some of FTNT’s cybersecurity peers and competitors, and as can be seen, several are growing far faster with better margins but at a sharp valuation premium in absolute and relative terms. The risk to FTNT is that, if it does not accelerate growth, it may see valuations continue to decline despite solid cash flow.

Created by author with data from Capital IQ

Valuation

The market price target is US$72 for YE24 which backs into an implied P/E target of 26x and PEG ratio of 2.1x which suggests that analysts are either assuming a potential pickup in growth or rewarding FTNT on its high cashflow generation and potential of capital returns via buybacks. All very positive but not congruent with a 2x PEG valuation in my view. I would venture to say that a 25x P/E may be challenging at projected growth rates into 2025 & 2026.

Consensus dispersion increases in 2025 and 2026, with the low-end far below medium as well as the high-end, which suggests that at least some analysts have very different views.

Consensus Valuation (Created by author with data from Capital IQ) FTNT Consensus (Created by author with data from Capital IQ)

Conclusion

I rate FTNT a sell. It’s a difficult analysis, given that much of the damage to the company’s valuation has been done, and the market is well aware of the decline in the products segment. However, I fear that the valuation discount may not be enough and the company’s “transition” to cloud-based services may meet with execution risk or increased competition.

Read the full article here