CarMax (NYSE:KMX) sounds like a great business on the surface. It’s the largest used vehicle retailer in the United States, poised to consolidate the fragmented used car market. However, investors will find that issues plague CarMax after closer examination. The current macro environment is unfavorable, SG&A spending is too high, and CarMax’s stock is overextended, given its underlying business characteristics.

Business Overview

CarMax can charge more than its competition for vehicles because of the customer experience. For example, sales reps are paid fixed commissions. This prevents the salesforce from steering customers towards vehicles with higher gross profits. CarMax is also known for its no-haggle pricing, which simplifies the purchasing process.

Selection is another reason why CarMax can charge extra. Customers can request that vehicles be transferred, and CarMax locations are much larger than other used vehicle retailers.

Other aspects of CarMax’s business include its vehicle wholesaling business. This allows CarMax to sell vehicles that don’t meet its quality standards. CarMax also has a vehicle financing arm, and it sells extended warranties to its customers.

Macro Picture

Rates and Inflation

Retail sales recently increased 0.7% month-over-month, beating expectations by 0.3%. This hot retail sales report indicates an inflation problem that needs to be solved by keeping rates higher for longer. Core inflation, which is still in the high 4% range, further confirms the existence of an inflation problem.

Currently, the market doesn’t expect rate cuts until mid-2024. Continuously elevated interest rates will be a headwind for used car sales during FY2024 because high interest rates translate into high car payments for the consumer.

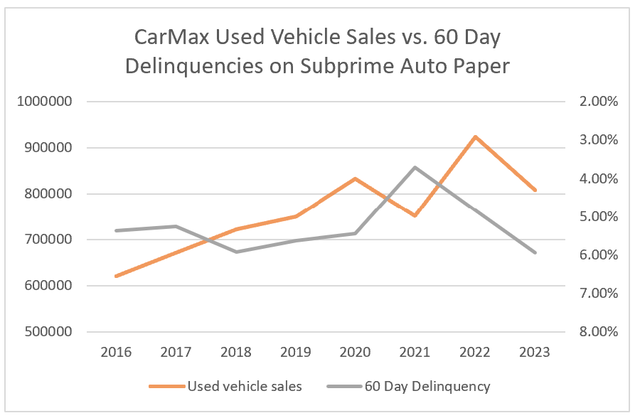

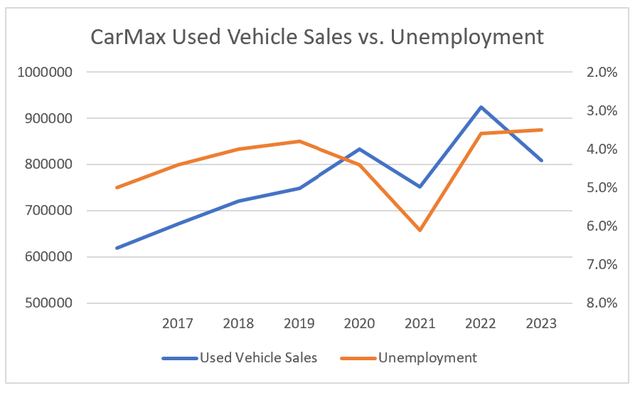

Unemployment and 60-day Subprime Auto Loan Delinquencies

Used vehicle sales tend to be negatively correlated with 60-day Subprime Auto Loan Delinquencies (S&P Global) Used vehicle sales tend to be negatively correlated with unemployment (S&P Global)

Unemployment is currently very low, whereas 60-day Delinquencies on Subprime Auto Paper are reaching new highs. If the economy falls into a recession and unemployment rises, used auto sales will get hit multiple times. Higher unemployment will reduce used car purchases made by lower and middle-class consumers. Also, 60-day delinquencies on subprime auto paper will rise if unemployment rises, cutting subprime borrowers out of the market (because lenders will demand higher interest rates). Additionally, CarMax will have to incur additional losses associated with repossessions.

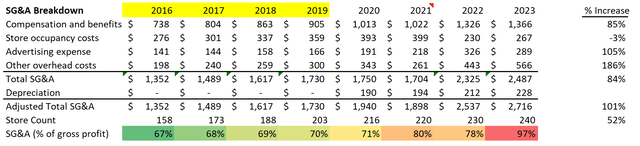

SG&A Analysis

CarMax Investor Relations

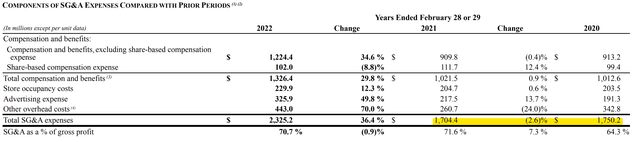

SG&A, as a percent of gross profit, increased consistently from 2016-2021 (making CarMax less profitable). I believe this can be attributed to the following factor noted in CarMax’s latest 10-K:

Competitors using online-focused business models, both for direct sales and consumer-to-consumer facilitation, could materially impact our business model. Increased online used vehicle offerings and the growing consumer trend of buying vehicles online could make it more difficult for us to differentiate our customer offering from competitors’ offerings, could result in lower-than-expected retail margins, and could have a material adverse effect on our business, sales and results of operations.

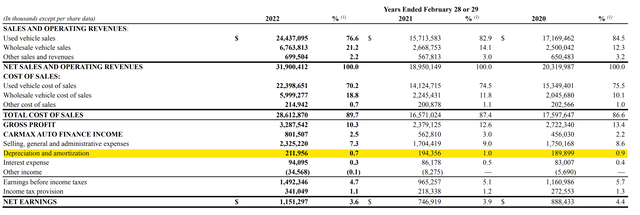

What’s more concerning is that SG&A increased sharply in 2022 after CarMax acquired Edmunds. Only $24.5 million of the $300 million compensation expense increase was associated with the Edmunds acquisition. The increase in advertising spend and other overhead costs were also not attributed to the Edmunds acquisition. It seems like management overspent during 2022, and their decisions have stuck with CarMax through 2023 (considering that SG&A is still elevated).

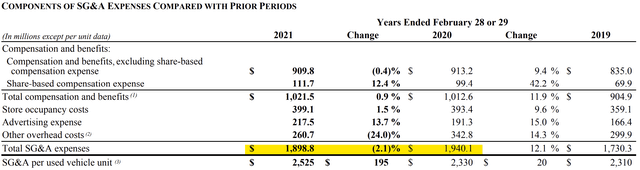

Additionally, investors may not have a complete picture of SG&A trends due to a recent accounting adjustment. Notice how SG&A changes from the 2021 10-K to the 2022 10-K:

2021 10-K (CarMax Investor Relations) 2022 10-K (CarMax Investor Relations)

The following note from the 2022 10-K explains that depreciation and amortization were separated from SG&A:

CarMax Investor Relations Depreciation and amortization are now a separate line item (CarMax Investor Relations)

Overall, I find it very difficult to expect management to deliver excellent performance, given their decisions regarding SG&A spend.

Relative Valuation

S&P Capital IQ

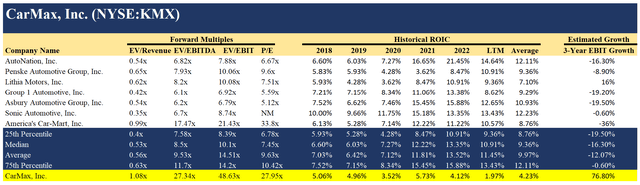

CarMax has the lowest average return on invested capital (ROIC) and the highest estimated EBIT growth compared to its peer group. This is usually not an ideal combination because growth destroys value when a company’s ROIC is lower than its weighted average cost of capital (WACC). CarMax’s WACC is 7.23% (which is higher than its average ROIC of 4.23%). In this case, the EBIT growth is beneficial because it’s driven by efficiency growth (getting more operating income out of stores) rather than reinvestment (building more stores).

Although CarMax is expected to grow EBIT quickly over the next few years, it still looks relatively expensive. Assuming that CarMax’s EBIT increases from $658MM to $1.6B (my 2026 EBIT estimate in the DCF further down in this article, which is higher than analyst estimates) overnight, CarMax would be trading at 19.44x EBIT. This would still leave CarMax as the second most expensive company in its peer group (on an EV/EBIT basis) while having the lowest ROIC.

I believe that CarMax should be trading between 10.1x-14.51x (between the median and average EV/EBIT of its peer group) its 2026 EBIT. This is because, in my view, CarMax’s low ROIC and above-average EBIT growth offset one another, making CarMax an average company.

S&P Capital IQ

Expected EV was calculated by multiplying EBIT by the expected EV/EBIT multiple. Using my assumptions, the value of equity is worth somewhere between $395MM and $7.7B.

Intrinsic Valuation

The following valuation uses very optimistic assumptions. Given my assessment that CarMax is significantly overvalued, even alongside optimistic assumptions, I believe that long-term returns from CarMax will likely be very low.

Daniel B. Wilson Daniel B. Wilson

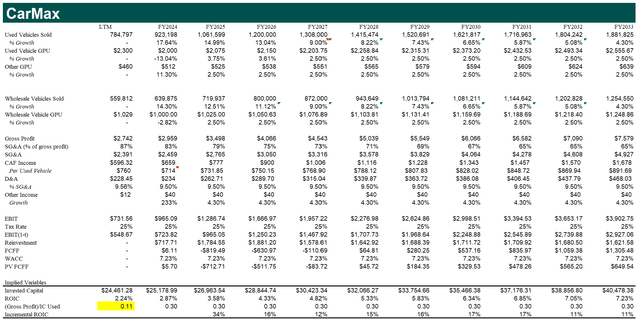

Used Vehicles Sold & Wholesale Vehicles Sold: I assume these numbers move linearly towards management’s estimate of 2 million total vehicles sold by 2026. Historically, 60% of CarMax’s vehicles sold have been used vehicles, and 40% of CarMax’s vehicles sold have been wholesale vehicles, so I used these percentages for FY2026. In FY2027, I assume growth reverts to 9% (roughly 2018/2019 vehicle sales growth) and slowly moves towards the risk-free rate (a proxy for the economy’s growth rate) as CarMax becomes a mature company.

Why do I think this assumption is optimistic? CarMax plans on opening only five locations in FY2024, putting them at 245 locations by the end of the year. In 2019, CarMax had 203 stores, meaning that the number of stores has increased by 18.23% since 2019. CarMax sold 748,000 vehicles in 2019, and applying this increase in store count puts them at 884,000 projected vehicles sold. To reach 1,200,000 used vehicles sold, CarMax would likely have to grow its store count by 35.7%, or 16.5% in FY2025 and FY2026. This is unlikely given that CarMax grew store count by 8-9% annually during 2017-2019.

Used Vehicle Gross Profit Per Unit (GPU): I assume GPU moves down to $2000 in FY2024 (roughly historical average) and then moves linearly towards management’s GPU estimate of $2100-$2200. Then I assume GPU grows at the rate of inflation (2.5%).

Other GPU & Wholesale Vehicle GPU: I used the recent historical averages for FY2024. Then, I assume these grow at the rate of inflation (2.5%).

SG&A (as a percentage of gross profit): I used management’s SG&A (as a percentage of gross profit) target of the mid-70s for FY2026. I project the current SG&A to approach the 75% target linearly. Then, I expect SG&A (as a percentage of gross profit) to move linearly towards its historical average of 65% over five years.

Why do I think this assumption is optimistic? It’s in the management’s best interest to give investors rosy predictions (because then shares go up, resulting in a bigger performance bonus for management). This means the 75% target may be a best-case scenario.

CAF Income: I used the recent historical average CAF per vehicle for FY2024. Then, I assume the CAF income per used vehicle grows at the rate of inflation (2.5%).

D&A: I used the 3-year historical average D&A as a percentage of SG&A.

Other Income: This is primarily the income from Edmunds. Edmunds was purchased in 2021 at an enterprise value of $404 million, so I assume they were bought at 10x their income (for simplicity). Other income then grows at the risk-free rate (I assume the business is mature). Most likely, their income is lower than this (other income was only $12 million during the last 12 months, but it was also mixed with CarMax’s other income). I chose a number that is probably too high in the spirit of my optimistic valuation.

Effective Tax Rate: 25% (worldwide average tax rate).

Reinvestment:(Change in Gross Profit)/((Gross Profit)/(Invested Capital))

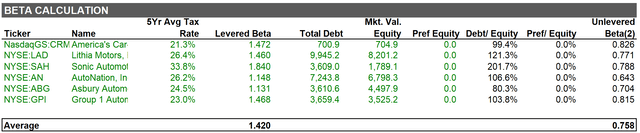

WACC: CAPM; Aswath Damodaran’s implied ERP of 4.83%; bottom-up beta; market value of debt; AA credit spread added to the risk-free rate for the cost of debt

S&P Capital IQ

(Gross Profit)/(Invested Capital) Ratio: The box highlighted in yellow is the LTM ratio. All the other ones are incremental ratios used to calculate reinvestment. I adjusted this until my year ten return on invested capital was equal to my cost of capital.

Why is this assumption optimistic? CarMax’s historical (Gross Profit)/(Invested Capital) ratio has been in the 0.1-0.2 range over the past decade (meaning that my reinvestment is probably too low. A higher ratio means less reinvestment is needed to generate growth). Additionally, CarMax’s ROIC has always been lower than its WACC from 2010-2020, so my assumption that CarMax’s ROIC will return to its WACC (within ten years) may be unrealistic.

Incremental ROIC:(Change in EBIT(1-t))/(Previous Year’s Reinvestment)

Why is this assumption optimistic? The used car business is highly competitive, with low returns, so CarMax is unlikely to take on projects that earn returns greater than its current WACC.

Risks

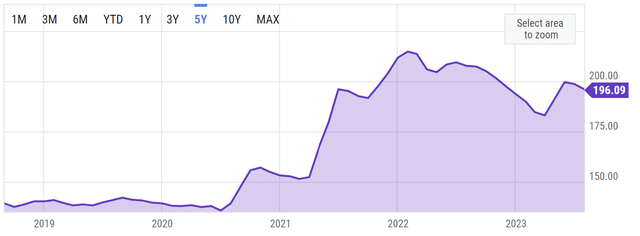

Used Car Prices Declining

CarMax Investor Relations Used Car Prices Over Time (YCharts)

Gross profit per unit tends to be independent of used car prices. This means that when used car prices fall, CarMax will be more profitable for the following reasons:

1. Used car prices falling will make cars more affordable for consumers, resulting in more sales

2. Gross profit per unit is typically $2100/car, regardless of used car prices, so the same gross profit per vehicle, and more sales, translate to greater profits

In summary, CarMax may beat analyst estimates if car prices fall.

Falling Interest Rates

If inflation slows, the Fed may cut interest rates sooner than the market anticipates. This will allow consumers to purchase more vehicles because the monthly payment on their loans will be lower.

Buybacks

Management may choose to resume buybacks if macroeconomic conditions improve. This has the potential to excite investors.

Conclusion

Even if the macro environment suddenly turns around, I see very little chance of equity outperformance. I believe CarMax will be perpetually held back by its low ROIC (which makes growth a bad option). On the short side, I see little to no fundamental risk – CarMax would almost certainly have to reinvent itself to justify current prices. I’ll be on the sidelines until the share price drops by 75%+ or until management takes on projects that generate returns greater than CarMax’s cost of capital.

Read the full article here