Investment Briefing

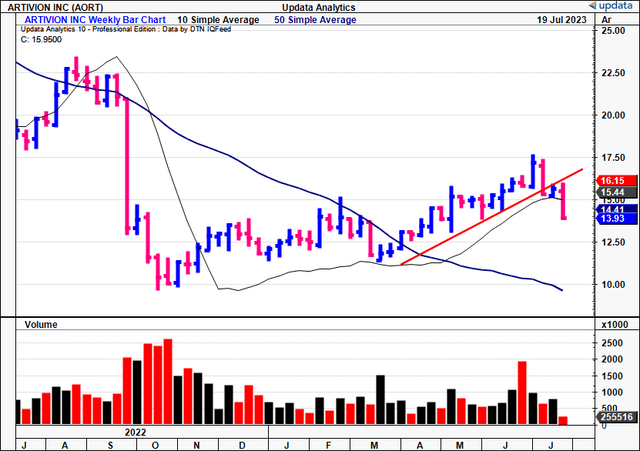

In the time since my April publication, the tides of change have arrived at the shores of Artivion, Inc.’s (NYSE:AORT) feet. Rewind back to midway through FY’22, there was sheer panic from investors after the company announced its PROACT mitral clinical trial had failed. Investors dumped the stock and rode it from ~$22.50 down to $9.60 in just 3 weeks of trade.

I’m the first to admit my hopes for AORT’s equity performance—not the company’s performance—were dashed at the time as well [I’d gone from a strong buy in May FY’21 to rating it hold by Q3 FY’22]. However, slowly but surely, the company has demonstrated its capacity to overcome the market’s short-term machinations.

AORT’s growth equation is fairly simple calculus. It is a function of 1) sales [inc. ancillary sales] of existing product lines, 2) obtaining new product approvals, and 3) adding reps to move product and get revenues through the door. With that in mind, I am turning far more constructive on the company moving forward, and I’ll run through my investment reasoning why in this report. Net-net, I have turned far more constructive on AORT, and am opening a position, eyeing $24 as the price target, 50% on the market price as I write.

Figure 1. AORT price recovery following FY’22 selloff instigated by PROACT failure

Data: Updata

Risks to investment thesis

Investors must understand the following risks that could nullify the investment thesis:

- We saw the sensitivity of the market to AORT’s trial updates last year. Any additional trial failures could result in a wide selloff.

- I have made first commitments to AORT since 2021, and a pullback of 12.5% in the stock price from my initial entry price would see me exit the stock (my stops are placed at this mark). If AORT were to rally further, a 12.5% pullback from the average range within the rally would see me stopped out. Why the rigid numbers on exiting the position? I am in the business of compounding, and, ultimately, protecting capital. The mathematics of investment losses vs. gains are asymmetrical, and rely too much on rapid recovery once there’s a downside move. I can always buy it back on a reversal if it were to collapse.

- There are obvious macro-level risks to consider. You’d be wise to consider the ongoing effects of the current rates cycle, inflation numbers, and the macro-level data that comes out each month that could impact equity markets.

- Various countries are experiencing strikes by healthcare/medical workers, which could slow the process of patient turnover for AORT, thereby crimping sales.

These should be recognized in full before proceeding, as mentioned.

Critical facts underpinning revised thesis

Based on events that occurred since the last publication, multiple talking points for discussion. In my opinion, based on thoughtful analysis of the investment facts, AORT’s recent progress has paved the way for a clearly defined growth trajectory. Still— some issues must be addressed first.

1. Addressing the elephant in the room: PROACT Mitral

It’s no secret that investors were rattled by the outcome of the PROACT trial. As a reminder, AORT begun the drug trial >10 years ago, and it missed the primary endpoint of stopping bleeding in thromboembolic events. AORT is still pushing for approval though. As I discussed in the last analysis: “…potential approval in H2 could be a meaningful tailwind to attract investment”.

And after extensively reviewing the critical facts to the debate, I would note the additional points:

- The standout for mine is AORT’s progress in growing its On-X mitral valve business. Hence, turnover/profits are booked from the valve’s sales.

- The PROACT 10A trial was a drug trial. The company was trying to optimize the compound, and it failed. In other words, that PROACT failed has little bearing to the outcome of On-X sales.

- AORT said it remains in constant dialogue with the FDA on getting PROACT Mitral approval, and, based on language on the last earnings call, it could potentially secure in H2 FY’23.

As Dinah Washington so eloquently sang, “What a difference a day makes”. Especially for AORT. An FDA approval for this segment would potentially reverse the outlook for its share price in my view, and claw back the bulk of losses endured last year (both are event-driven reasons for the change in stock price, after all). Further, should AORT get FDA approval for PROACT Mitral, it shows that patients with the On-X valve in situ could safely be maintained at lower anticoagulation levels than the current standard of care. Critically, none of the company’s financial projections include the approval of PROACT Mitral, so it could be a meaningful tailwind if approved.

2. PerClot approval

Adding to the short-term momentum was the FDA’s premarket approval (“PMA”) of AORT’s PERCLOT Haemostatic System (“PerClot”) in May. The system has label approval for use in various laparoscopic surgeries, to control intra-surgical bleeding. As a reminder, AORT sold the PerClot franchise to Baxter (BAX) back in FY21, entitling it to various milestone payments in the process.

Now with the PMA, the company will send off PerClot inventory, and receive $14.3mm in milestone payments in doing so. It will have received $44mm from BAX after this, with further entitlements of up to $10mm more by FY’26 based on certain milestones. Given the approval [plus other factors], management updated its revenue forecasts to $348mm at the upper end of range, calling for 12% YoY growth.

Further on the regulatory and pipeline font, AORT is also sporting the AMDS and PERSERVERE trials. In the PERSEVERE arm, AORT is investigating whether patients with acute DeBakey Type I aortic dissections can be safely treated using its AMDS Hybrid Prosthesis. It has successfully enrolled 51 patients across c.30 centres, all in the U.S. The trial will assess:

- Reduction in all-cause mortality

- New disabling stroke

- Myocardial infarction (“MI”)

- New onset renal failure (only those requiring dialysis), and

- Re-expansion of the true lumen of the aorta.

The company expects complete enrollment in H2 this year, and, assuming the trial meets its endpoints, anticipates receiving FDA approval for its AMDS device in 2025.

3. Attractive growth in core business

AORT is producing qualified growth in its legacy business lines, made primarily of On-X valves, BioGlue tissue valves, and aortic stent grafts. Thinking in first principles, On-X is the major breadwinner. Per AORT, it is the “market-leading mechanical valve in the U.S.”, being the “only valve that has a low [international normalized ratio] INR”.

Critically, On-X valve sales have compounded at a 5-year average of 13—14%, and management had guided ~15% geometric growth in their upside case going forward. However, Q1 FY’23 On-X sales came in at 24% YoY growth, nearly double the 5-year average. The jump was all demand-driven as well, no major contribution from pricing, and that is good to see. It is a testament to the company’s sales reps and their productivity— great info moving forward. The remaining portfolio was up 3—7%, nowhere close to On-X’s performance.

These numbers were bolstered by exceptional regional demand in Latin America (“LatAm”) and APAC:

- Total revenues from LatAm were up 36% YoY last period

- Meanwhile APAC revenues were north of 17% to the upside, driven primarily from new product approvals, whereas the addition of new reps in both territories drove sales in both regions. The company expects similar trends moving forward.

- This contrasts to its Europe market, down 100bps on the year.

I’d also add that AORT’s partner, Endospan, is progressing with its NEXUS aortic stent graft system. The graft has investigational device exemption (“IDE”) status, and is being examined in the TRIOMPHE trial. Currently, 80% of enrolled patients have been treated [n=44]. The firm is aiming for PMA aby 2025.

Assume all of these updates go perfectly according to plan—FDA approval of AMDS, PROACT Mitral approval, then NEXUS in 2025—management estimate this could increase the company’s market opportunity by an estimated $900 mm.

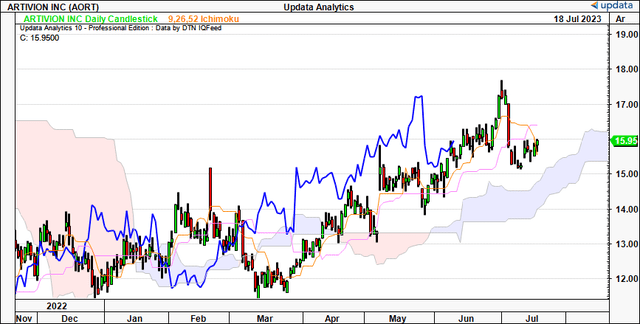

4. Market generated data supportive

Technicals governing the AORT share price are equally as supportive of a further re-rating in my view. Based on Figure 2, the cloud chart below, trends are still bullish. It shows the price line and lagging lines trading above the cloud, with additional upsides to $16.50 by the end of July a possibility. It also shows there is downside wiggle room whilst still remaining on bullish trend. You’ll also note the last time AORT tested the cloud base in May, it swiftly bounced from this mark and set new highs. This is handy to know moving forward.

Figure 2.

Data: Updata

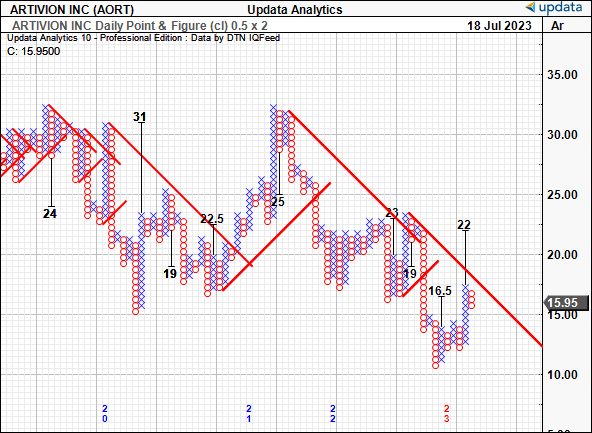

Additional confluence is observed via the point and figure studies below. These studies remove the noise of time and also the intra-trend volatility flutters to form a more objective directional view. With the latest price thrust from May, we’ve got upside targets to $22, even with the latest short term pullback. It supports the notion above that we are still on bullish trend for the time being. Note, the study saw the $16.50 mark earlier, and the $19 level before that, and this adds a layer of confidence.

Figure 3.

Data: Author

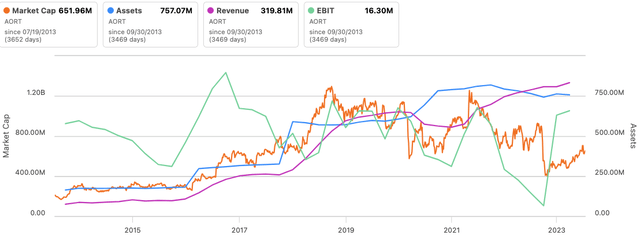

Valuation and conclusion

The market values AORT as a function of profitability and thus returns on its capital investments [Figure 3]. Prior to 2018 [in the period of 2013—’18 in the series below] it was valued on the basis of sales and asset factors. This makes sense, as the company places its valves/stents for use within surgery, and thus, profitability is key to see AORT trading as a going concern. Sales alone won’t do it.

In that vein, management’s updates EBITDA guidance of $52mm is attractive in my view, especially that AORT’s equity stock trades at 18.7x forward EBITDA. I am aligned with management’s assumptions, and valuing AORT at 18.7x forward gets me to ~$24/share on those estimates.

This supports a buy rating. I am thus allocating my first commitments to AORT since mid-2022, to purchase 625 shares at scaled market orders of $15.95—$16.50/share. I won’t enter beyond that mark. I am looking to an initial price objective of $24, as mentioned, otherwise 48% upside potential ($7.75/share) from my intended average purchase price of ~$16.25. So I’d be looking to pay $15.95—$16.50/share for ~$7.75/share in return on top of this.

Figure 4.

Data: Seeking Alpha

In summary, the investment facts are far more constructive for AORT’s equity performance downstream than they were a year ago. Looking ahead, the firm has demonstrated its capacity to grow core business operations, whilst building out its pipeline. The PROACT Mitral division is still in hot contention, and an FDA approval would be a meaningful tailwind, not in the least on the investor sentiment front. Wall St analysts have made 5 upward revisions to forward sales in the last 3 months, and that’s saying something in my view. This, and the outsized growth in On-X, with 15% CAGR projections moving forward, is also supportive of this viewpoint. Net-net, I am looking to buy 625 shares and searching for $24/share or 50% upside potential from today’s market value. Revise to buy.

Read the full article here