Dear Investors,

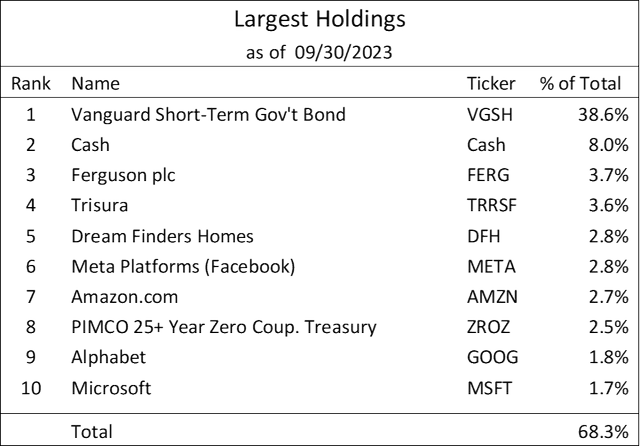

As a reminder, I will no longer be reporting performance publicly based on recent marketing regulations issued by the state of NC. Year-to-date, the S&P 500 (SP500, SPX) returned 13.1%. We ended the quarter with 38.6% of the portfolio in cash and short-term government bonds. The recent increase in 10-year Treasury rates has led to a re-pricing of many assets, including equities, real estate, and private equity-backed companies. While debt has re-priced, the other shoe to drop is the actual dent to cash flows as a result of refinancing debts at higher rates, which even if multiples stay constant, should lead to a slow grind sideways or lower over multiple years as these refinancings occur. It has already hit firms with floating rate debt, and those with fixed rate debt will face the same challenges, but on a lag.

EXISTING PORTFOLIO ACTIVITY

Sold: None

Bought: LESL, OTCPK:TRRSF, POST

Valuations got more attractive during the quarter, and as a result we added to a number of existing positions. Starting with Leslie’s (LESL), I continue to believe pool services are essential for those who own them. At its current 6.5x multiple of forward free cash flow, LESL should look to pay down debt and repurchase shares. I’ve seen healthy companies become unhealthy by wasting precious capital on buybacks when they should have been allocating some capital to reducing debt. I hope LESL management does not make the same mistake. If they simply pay down debt from cash flow, they will generate significant equity value.

Trisura (OTCPK:TRRSF) remains one of my favorite investments, despite a notable failure earlier this year related to an unrated reinsurance partner defaulting on its obligations to Trisura. As a result, Trisura took a notable equity charge and set itself back somewhat. Trisura has since strengthened its balance sheet, and trades at an attractive 12.5x P/E multiple with years of future growth ahead of it.

Finally, I added to Post Holdings (POST) because it is a long-term position that was undersized, and POST had recently announced a large acquisition of pet food brands that act as a new platform. POST is turning back to the clock by creating a reincarnation of Ralston-Purina, the conglomerate Bill Stiritz ran many years ago with great success. Like Stiritz’s Ralston, POST has been a consistent purchaser of its own shares, demonstrates improved efficiency within its own businesses, and occasionally makes disciplined acquisitions to bolster existing franchises or add new platforms. Additionally, POST is not an empire builder, as it has sold its private label food business to a private equity firm, and spun off BellRing Brands in recent years. With the spinoff of WL Kellogg in recent days, and due to Kellogg’s lower margins, I would be surprised if POST does not try to acquire some portion of WL Kellogg, although it would likely need to divest some cereal assets to avoid regulatory scrutiny. POST trades relatively inexpensively, at a 9.1x EV/EBITDA ratio, and means that POST is positioned to continue its unique value creation going forward.

NEW PORTFOLIO ACTIVITY

Bought: BURL

Burlington Stores (BURL) participates in the off-price retail category and competes against well-known players such as TJ Maxx and Ross Stores. BURL recently suffered from an inventory overhang that dented margins and is also suffering from a slowdown in same store sales. With that said, the company has capacity to double its stores, double its margins to levels consistent with peers, and expand same- store sales growth. On normalized margins, which the company last achieved in fiscal 2019, BURL is trading at ~10x earnings, with potential to grow top-line low double digits, increase bottom line mid- teens, and increase EPS high teens over time.

CONCLUSION

Recent news showing declining inflation has been welcomed by markets as a sign that interest rates are likely headed lower in the not-too-distant future. The only scenario where interest rates decline in the near term is if we face a recession, in which case equities will probably not be spared. There are lagged effects of higher interest rates that have not yet hit, and if the Fed gets what it wants in the form of lower inflation, it likely means some economic pain for all of us. We have a handful of companies we’d like to own at lower prices, and we’re waiting for the opportunity to buy. In the meantime, we remain very conservatively positioned to take advantage of those opportunities.

Until January,

Argosy Investors

APPENDIX

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here