Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

Based on data compiled by Credible, mortgage rates for home purchases have fallen across all key terms since yesterday.

Rates last updated on May 11, 2023. These rates are based on the assumptions shown here. Actual rates may vary. Credible, a personal finance marketplace, has 5,000 Trustpilot reviews with an average star rating of 4.7 (out of a possible 5.0).

What this means: Mortgage rates have fallen across all key terms. Rates for 30-year terms have fallen the least and edged down to 6.49%. Meanwhile, both 15- and 20-year terms saw slight decreases in their rates, hitting 5.625% and 5.875%, respectively. Rates for 10-year terms have fallen the most, dropping by over a quarter of a percentage point to 5.625%. Homebuyers looking for a smaller monthly payment should consider 20-year terms over 30-year terms, as their rates are over a half of a percentage point lower. Borrowers who would rather maximize their interest savings should instead choose either 10- or 15-year terms.

To find great mortgage rates, start by using Credible’s secured website, which can show you current mortgage rates from multiple lenders without affecting your credit score. You can also use Credible’s mortgage calculator to estimate your monthly mortgage payments.

Based on data compiled by Credible, mortgage refinance rates have fallen across all key terms since yesterday.

Rates last updated on May 11, 2023. These rates are based on the assumptions shown here. Actual rates may vary. With 5,000 reviews, Credible maintains an “excellent” Trustpilot score.

What this means: Mortgage refinance rates have fallen across all key terms. Rates for 20- and 30-year terms have edged down, hitting 5.75% and 6%, respectively. Meanwhile, rates for both 10- and 15-year terms have fallen by a quarter of a percentage point, dropping to 5.625% and 5.375%, respectively. Homeowners looking to refinance to save the most on interest rates should consider today’s lowest rate, 15-year terms at 5.375%. Borrowers who would rather have a smaller monthly payment should consider 20-year terms, as their rates are a quarter of a percentage point lower than those of 30-year terms.

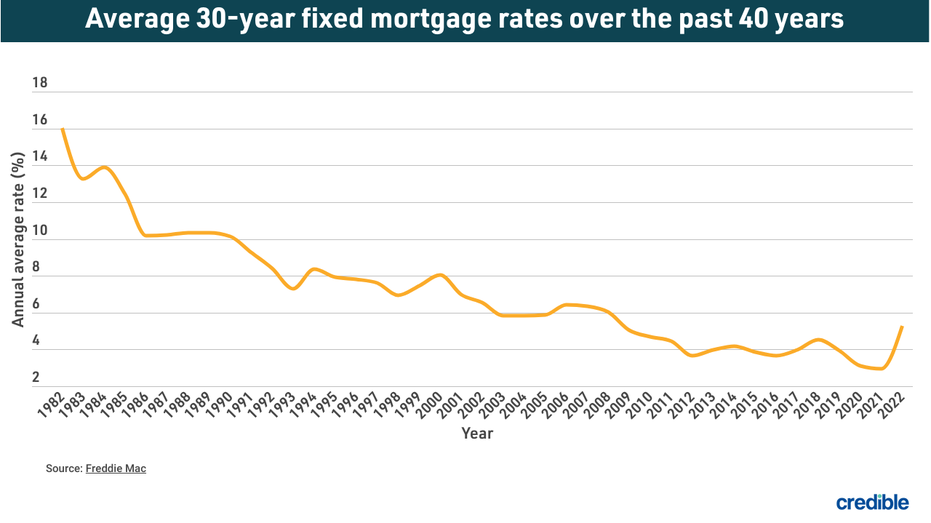

How mortgage rates have changed over time

Today’s mortgage interest rates are well below the highest annual average rate recorded by Freddie Mac — 16.63% in 1981. A year before the COVID-19 pandemic upended economies across the world, the average interest rate for a 30-year fixed-rate mortgage for 2019 was 3.94%. The average rate for 2021 was 2.96%, the lowest annual average in 30 years.

The historic drop in interest rates means homeowners who have mortgages from 2019 and older could potentially realize significant interest savings by refinancing with one of today’s lower interest rates. When considering a mortgage or refinance, it’s important to take into account closing costs such as appraisal, application, origination and attorney’s fees. These factors, in addition to the interest rate and loan amount, all contribute to the cost of a mortgage.

How Credible mortgage rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates reported in this article are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 700 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates reported here will only give you an idea of current average rates. The rate you actually receive can vary based on a number of factors.

How does the Federal Reserve affect mortgage rates?

The Federal Reserve System — or “The Fed,” as it’s commonly called — is the United States’ central bank. It’s tasked with taking steps to keep the economy safe, stable and flexible. Consequently, the Fed controls the U.S. money supply and short-term interest rates, and sets the Fed funds rate, which is the rate that banks apply when borrowing from each other overnight.

But the Fed doesn’t actually set mortgage rates. Rather, multiple things the Fed does influence mortgage rates. For example, while mortgage rates don’t mirror the Fed funds rate, they do tend to follow it. If that rate rises, mortgage rates typically rise in tandem.

The Fed also buys and sells mortgage-backed securities, or MBS — a package of similar loans that a major mortgage investor buys and then resells to investors in the bond market. When the Fed buys a lot of mortgage-backed securities, it creates demand in the market, and lenders can make money even if they offer lower mortgage rates. So rates tend to be lower when the Fed is doing a lot of buying.

When the Fed buys fewer MBS, demand falls and rates will likely rise. Similarly, when the Fed raises the Fed fund rate, mortgage rates will also increase.

If you’re trying to find the right mortgage rate, consider using Credible. You can use Credible’s free online tool to easily compare multiple lenders and see prequalified rates in just a few minutes.

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.

Read the full article here