Main Street Capital (NYSE:MAIN) seems one of the most coveted BDCs on the Street as the company has delivered consistent net asset value per-share growth over the life of the company. While Main Street consistently handed dividend raises to its shareholders, the BDC seems overpriced with a 58% premium to net asset value… which I believe translates to an unattractive risk profile for dividend investors. The BDC’s shares are paying an 8% yield, while Main Street’s core LMM portfolio generated a much higher weighted-average debt yield of 13% in 2023. I believe the premium is still very high, but the dividend at least is very well-protected!

Previous rating

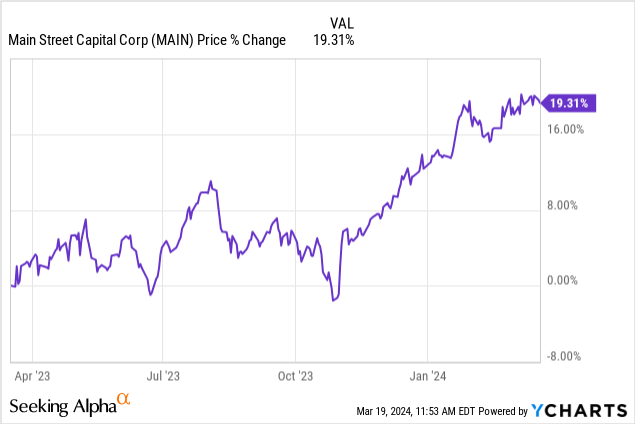

I worked on Main Street in May 2021 which is when I rated the BDC a sell. Main Street’s shares did perform well since, however, and have increased 19% in price. Considering that Main Street managed to grow its net asset value at stronger rates than other BDCs in the last three years, I believe a rating upgrade to hold is justified.

Main Street achieved record income results in FY 2023

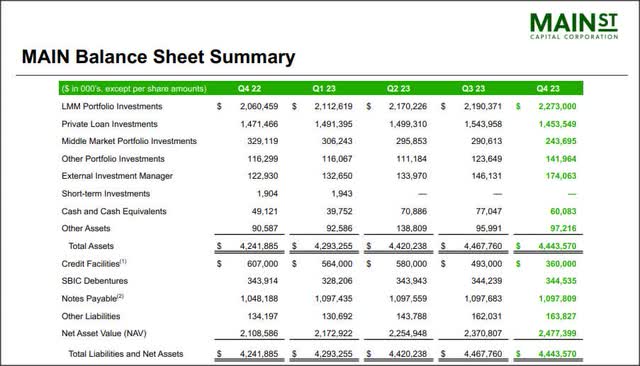

Main Street is a BDC with significant investments in (lower) middle market loans. These loans, which are chiefly handed out to companies with proven business models and predictable cash flow, had a combined value of $2.27B as of the end of FY 2023 while complementary investments (private loans) had an investment value of $1.45B and middle market loans were valued at an additional $243.7M. The BDC’s total fair value investments calculated to $3.97B in FY 2023. Across its portfolio of loan investments, Main Street achieved weighted-average debt yields ranging from 12.5% (private loans) to 13.0% in the lower middle market loan group.

Main Street Capital

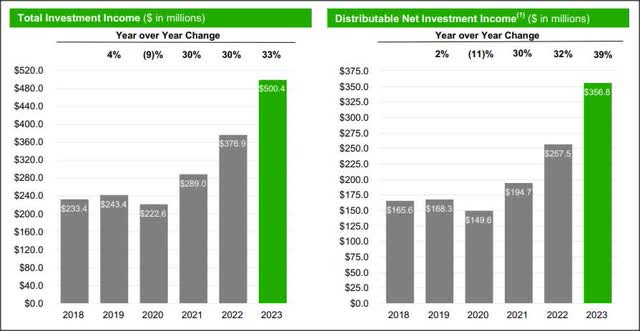

Main Street had a record year in FY 2023 and the BDC entered FY 2024 with considerable net investment income momentum. Last year, Main Street achieved record total investment income of $500.4M, showing 33% year over year growth. Main Street’s distributable net investment income also hit a record at $356.8M, showing 39% Y/Y growth, and it was the second straight year of distributable NII growth acceleration due to a strong comeback from the pandemic period.

Main Street Capital

Distribution coverage analysis

Main Street has earned a reputation chiefly for two things: 1) It’s ability to grow its monthly dividend, and 2) To provide a safe dividend that can be paid during good and bad times in the market.

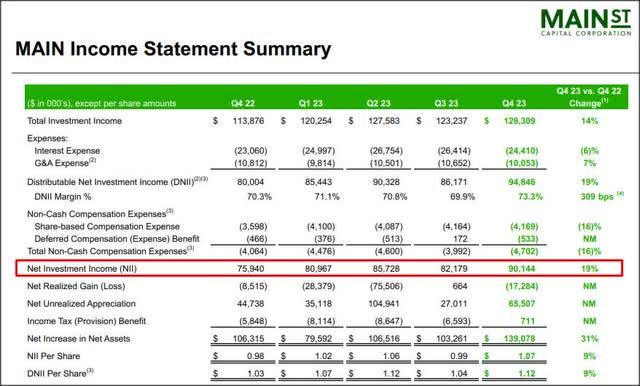

Main Street’s net investment income soared in FY 2023, in part because the Federal Reserve’s tightening policy resulted in a boost to the company’s net investment income. Main Street generated $90.1M in Q4’23 in NII (+19% Y/Y) and $1.12 per-share (+9% Y/Y).

The BDC distributed a total of $3.695 per-share last year, including four supplemental cash dividends amounting to $0.95 per-share. Main Street’s distribution coverage ratios in FY 2023, FY 2022 and FY 2021 were 1.17X, 1.17X and 1.10X, implying that the dividend safety margin in the last two years especially improved, despite payments of extraordinary cash dividends. From an income perspective, I think Main Street provides a very safe 8% dividend (and the BDC’s monthly dividends are growing), but I continue to have a problem with Main Street’s very inflated valuation that I don’t believe is justified.

Main Street Capital

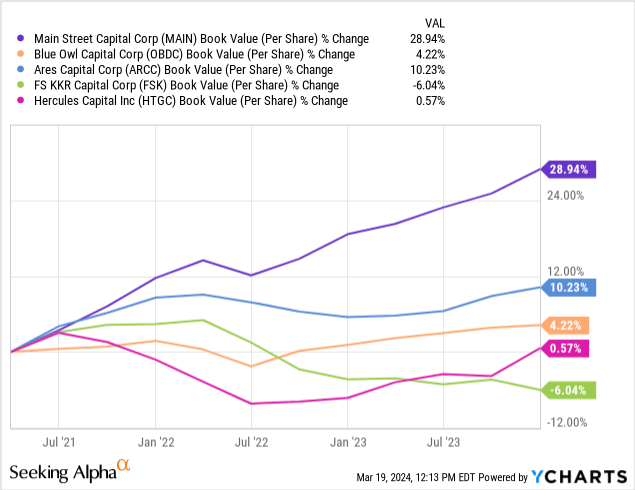

Better than average NAV growth

Main Street has the price of a premium BDC… and the NAV track record to support such a pricing. While the dividend is reasonably safe based off of the BDC’s distributable net investment income, I believe that the company’s results in terms of growing net asset value are respectable. In the last three years, Main Street has been able to grow its net asset value the fastest and achieved a 3-year NAV growth rate of 29%. Even Ares Capital (ARCC) and Hercules Capital (HTGC) have delivered much weaker NAV growth rates during this time…

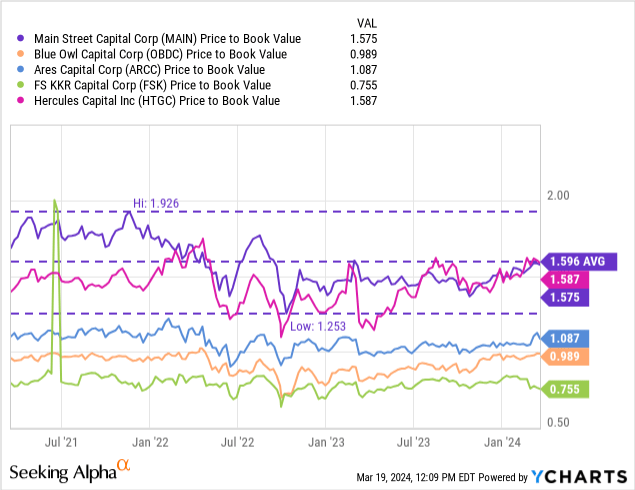

The result of this stronger NAV growth is that Main Street has one of the highest NAV premiums in the market: 58%. Only Hercules Capital is slightly more expensive than Main Street... and I continue to have a favorable opinion about HTGC because management is distributing a lot of cash to shareholders (quarterly standard + extraordinary), although shares are also expensive.

The result of this large premium is that Main Street’s dividend yield is just 8% while the loan portfolio generates a yield of 13%. I also believe that Main Street, given its 3-year average P/NAV ratio of 1.60X is about fairly valued here and I see limited upside for dividend investors.

Risks with Main Street

The risks with Main Street don’t relate so much to the BDC’s portfolio of LMM loans, but mostly to the company’s net asset value premium. Dividend investors continue to pay a very rich premium here, and as soon as Main Street’s investment returns falter, Main Street may have a much harder time defending its NAV premium. However, the dividend is fairly safe, and as the distribution coverage analysis has shown, the BDC retains considerable potential to grow its distribution going forward.

Final thoughts

Main Street generates durable dividend income from its portfolio of lower middle market loans, but the premium to net asset value is one of the highest in the market, indicating that dividend investors are fully pricing the BDC’s income potential. Yes, the dividend is well-supported by distributable net investment income and the company has achieved record results in FY 2023, but the current yield on the shares is only 8% while the portfolio yield for its middle market investments is a massive 13%. This yield difference is explained by the premium that investors place on the BDC’s dividend stream. While Main Street is as solid an income play as they come, I am still put off by the BDC’s high valuation. I do recognize, however, that Main Street has generated stronger NAV growth in the last three years than one of the largest BDCs in the market and therefore I am upgrading Main Street to hold!

Read the full article here